Stimulation Fintech Developments in Brazil

CRUCIAL ROLE OF CENTRAL BANK

eyesonbrasil

Amsterdam, April 12, 2023– The Brazilian government and the Central Bank have facilitated the growth of FinTech by implementing new supporting laws and policies. FinTech is the use of technology for financial services and products in any financial field. In practice, this means that companies will provide their financial services in technology ranging from online on the web, digitally on mobile devices, to the use of artificial intelligence. FinTech is often used and praised for its efficiency (many things can be done online or through be done on an app rather than in person), convenience and the potentially lower cost of not requiring a physical infrastructure.

However, there are challenges, such as the threat of hackers, lack of clear regulatory oversight (few laws on FinTech, especially on privacy) and how to engage consumers unfamiliar with the technology. Brazil’s São Paulo financial sector is the financial heart of Brazil (and the South American continent) with many of the international companies in the city of twelve million.

Data from the World Bank’s World Development Indicators shows that there are 113 cell phone subscriptions for every 100 people in Brazil (2017). It is the largest economy in Latin America and the ninth largest economy (GDP: USD 1.93 trillion according to the world’s authoritative IMF DataMapper. The World Bank’s Global Findex, which aims to promote financial inclusion, for 2017 presented the following information:• 70% of Brazilian adults have a bank account with a financial institution or a mobile bank account.Of the 30% of Brazilians who do not have a bank account, 24% have a mobile phone, which is almost 50 million people;• The percentage adults with a mobile phone in Brazil is 85%.

Related Posts:

Currently, Brazil’s financial market is dominated by four national banks – Itaú, Bradesco, Banco do Brasil and Caixa Econômica Federal, which held 76.35% of deposits in 2018 and similar concentrations were found on the area of credit and assets

The banks have started to innovate in FinTech and/or acquire FinTech companies. Another characteristic of the Brazilian market is the high interest rates that traditional banks charge on loans and credit cards; they are higher than in most countries with percentages above 50% [2]. In addition, owning a credit or debit card in Brazil is expensive.

These two conditions along with the aforementioned financial inclusion information set Brazil apart from other countries in the world. A report from Goldman Sachs (Fintech’s Brazil Moment) expects a potential FinTech revenue of more than BRL 75 billion (approximately EUR 20 billion) in Brazil over the next ten years.

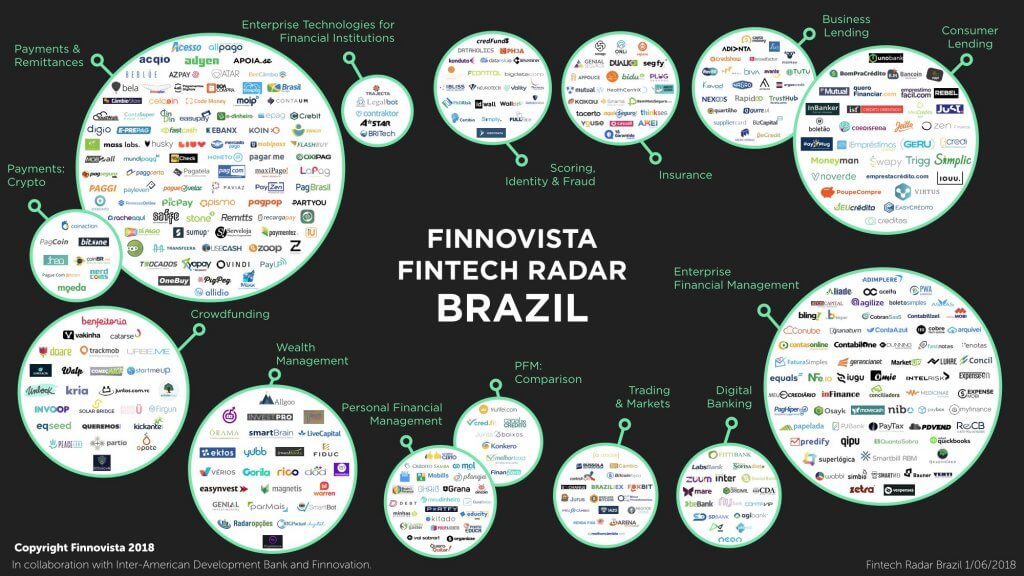

Brazil’s FinTech ecosystem

According to a mapping done by Finnovista1, there are a total of 377 fintechs spread over 12 territories in Brazil, the largest being Payments and Remittances (electronic money transfers), Enterprise Financial Management (organizing financial data for companies), Consumer and Business1 A Spanish fintech platform founded by entrepreneurial professionals from diverse backgrounds with the aim of leveraging the interest of entrepreneurs in digital transformation to create better financial services.

eyesonbrasil